Oil & Gas - where do we go from here?

The world seems to be caught in no mans land, but not all hope is lost in the energy world.

Oil and gas drive the world. Every time I think that I understand the full scope of:

How much a country relies on it (hint - alot!)

What is a by-product of natural gas and crude (hint - alot!)

What it is a key input into (also alot! From Aspirin to Lipstick)

I am reminded of where the world actually is on the energy continuum - despite all the fancy headlines about the energy transition.

Consider this:

Urea and Ammonia are two nitrogen-based fertilizers that are produced in large quantities and have shown to have dramatic increases in crop yields across the world. During the processing of natural gas, some are used for heat and electricity production, while the remainder is commonly used to create two by-products - Ammonium Nitrate and Urea, which are mixed with other ingredients to create widely used fertilizers. In fact, the use of these fertilizers is up 50% higher in some places than a decade ago.1

So when we have issues affecting the price of natural gas, like say, a war - this does not just impact cars and homes, but impacts things like the Urea price below, which impact food prices, which impacts - well, you get it.

Historical Urea prices

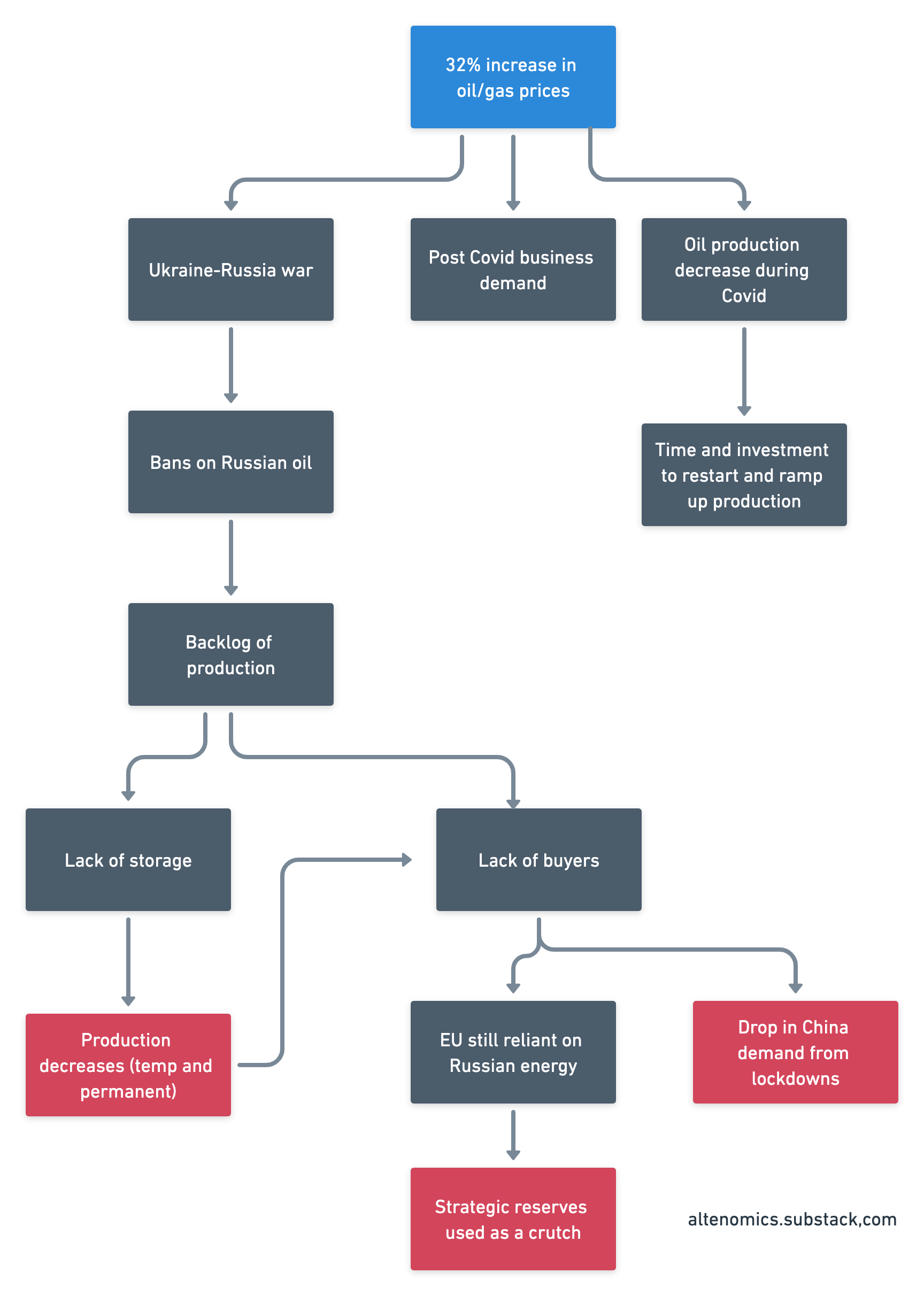

I've never really been an energy guy - which may be somewhat ironic given that I live in the great north of Canada. In the post last week about inflation, we saw that the March energy index was up 32% - hardly ideal for the dealings of the world unless you are an energy producer or supplier of course. For retail consumers and most other industries, this is bad news, if not entirely unsustainable. I decided to break my energy block, and finally take a solid dive. Here, we break down what is driving this change, what impacts this will have, and where we might go from here.

This is how I am thinking about it.

Effectively, while consumer demand is rising, and oil and gas producers are ramping up to meet that demand (and even more incentivized now), the Russian-Ukraine war is obviously driving up a majority of the price gain, but as we dive deep into this - the key reasons (in red) is why. This breaks down to 2 main things:

Lack of buyers

Lack of storage

The lack of storage sort of circles back to the lack of buyers. We know the world has been told to sanction Russian oil, but as we see in our McDonald’s example below, what does that actually mean?

Who is going to buy Russian oil?

There are 3 main components to this thought. Bargain hunters - who are looking to capitalize on a discount with some deep value, there is the impact of China’s reduction in demand and the whole EU's reliance on Russian energy.

The bargain hunters

Look - I am not pro-anything that is happening here, but the thing is - this Russian oil has to go somewhere. Bans and economic sanctions - they change who purchases, or maybe when, but it doesn’t change the fact that there is some oil out there that needs to be sold. It is an artificial externality on the price, rather than a systemic issue (e.g not enough production available).

It is like McDonald’s having a sale because the president encouraged many people to go on a diet. Some, not all will listen to this.

As this saga goes on, we see a big drop in the discount of Urals (the name for the oil mix exported by Russia) to others such as Brent - the chart below shows this2.

Basically - for obvious reasons, Russian oil, a key input into so much, is for sale.

It’s not that simple of course, but as you can imagine, some nations may be less weary than others in picking up a good deal, no matter what it looks like. At the time of writing, Russia has been selling some additional oil to countries such as India and Turkey.3 I would expect more deals like this to happen, both by official and unofficial channels (countries avoiding reputational damage).

Chinese demand - on the bench

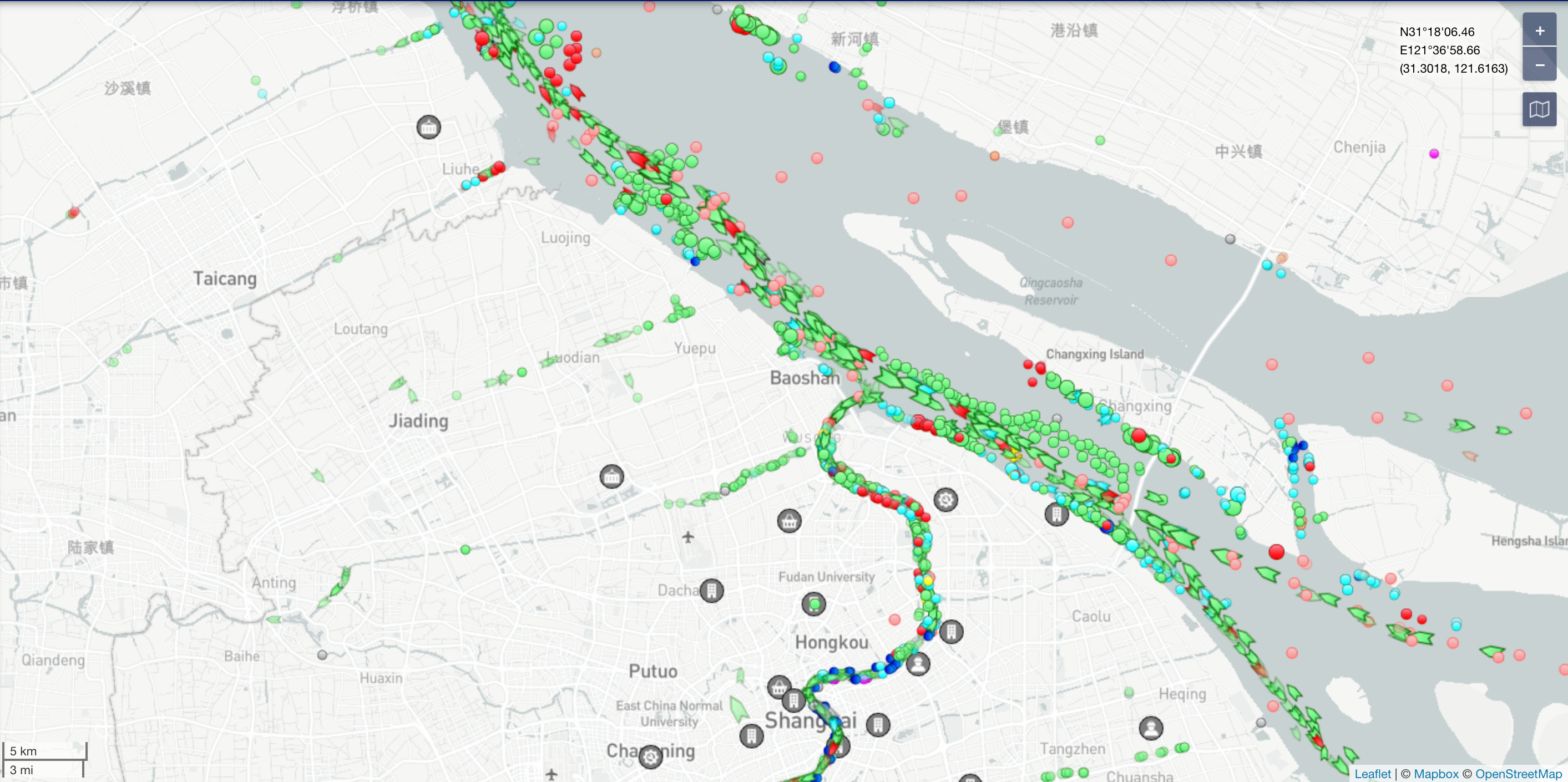

On the other hand, China is experiencing additional COVID lockdowns at the moment, hampering its demand for oil as manufacturing continues to slowly emerge again. If you really want to see how bad these lockdowns are, and their impacts, I am going to show you 2 things.

#1 - this thread. Just read it.

#2 - Shangais’s ports from satellite shipping data and the current increase in waiting time (adding to an already long time)

Demand for consumers is one thing, another is security. China is the world's largest oil importer and is the top buyer of Russian crude at 1.6 million barrels per day, half of which is supplied via pipelines under government-to-government contracts.

Seeing the potential issues of this disruption, some Chinese state-owned companies are looking at investments in some of Russia’s oil companies and Chinese officials have also prioritized purchasing additional oil as a security measure.

The current narrative is that China's state firms are expected to honor its long-term and existing contracts for Russian oil but steer clear of new spot deals.

Since the start of the war:

Basically - it’s a potential deep value play for many - but it remains to be seen if it’s a value trap, so everyone is cautiously investigating. China will look to carefully maintain a friendly narrative with other countries, but you can be sure that the last thing they would want is an overreliance on US oil - at the permanent cost of one of their critical energy partners - with established infrastructure.

“Export capacity is growing, too. The U.S. could be able to ship more than 800 million metric tons a year of liquefied natural gas by the end of the decade, up from 460 million metric tons currently” - Baker Hughes CEO Lorenzo Simonelli

This quote is encouraging to some but very threatening to others.

I think the question is when, not if, other parties will buy Russian oil. Many players seem to be avoiding purchasing in open tenders, or places where they might get some negative press - but the interest is there, and when that kicks in, amid the backlash, I can see a drop

It’s just not that simple to impose blanket sanctions, and eventually - countries will do what is in their best interest, which will affect outcomes.

EU reliance and an attempt to take the market

There are two sides to this - countries that will restrict exports of their oil in order to protect themselves, like Indonesia, and others that see this as a massive opportunity to export more and increase production at sky-high prices, such as the US.

The EU is getting caught in the middle. They need this oil and gas, nay, they rely on it. They would, as a whole, hoard their own oil - but let’s look at the top 3 producers in the EU.

#1 Russia - 10,499,000 BPD

#2 Norway - 1,861,000 BPD

#3 UK - 765,000 BPD

Yep. That’s a problem.

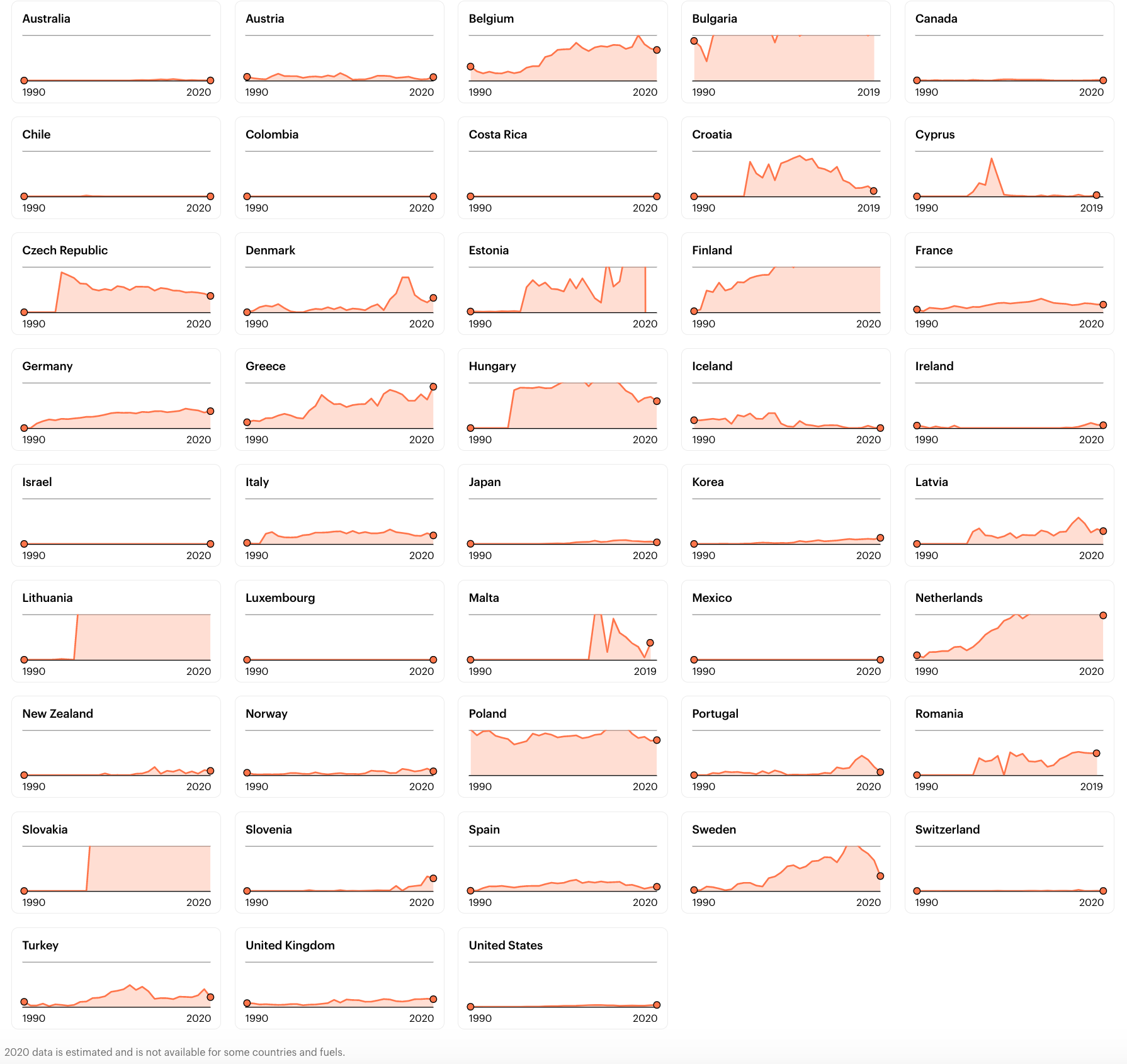

These charts below show the reliance on Russian oil as a % of total energy use. Data is from 2020, but paints the picture we need here - naturally, not all countries are pictured here due to data availability.

It is easy to put pressure on someone else (US → EU) when that is not your situation.

This is why Germany took so long to make a statement, which they just did - based on the power of the narrative - you can read more about this here (a fantastic read).

When you have Russia halting your gas supply (as they did to Poland and Bulgaria - see the chart above) - these things can be absolutely crippling, which is why they can even demand payment in rubles.

In the meantime, power plays will be made to try to take a bigger slice of the global market.

“Export capacity is growing, too. The U.S. could be able to ship more than 800 million metric tons a year of liquefied natural gas by the end of the decade, up from 460 million metric tons currently” Baker Hughes CEO Lorenzo Simonelli said in a recent article with E&E News

In the meantime - IEA has proposed a “10 point plan” to reduce EU reliance on Russian oil. You can read it here. Spoiler - a whole bunch of fluff that is not going to make a difference in the next few years - basically spend more money, be more energy-efficient and stop doing business with Russia. Have fun telling Poland “no new contracts with Russian oil and gas companies” when they have close to a 100% reliance.

Reflexivity - the players in action

When we think about reflexive action, it’s really saying that the game is dynamic - rules continue to evolve, and the players in the game can influence the outcome - they are not passive observers.

A quick example…

Oil prices go up → EU countries experience price shocks → Population is unhappy → Officials introduce some sort of subsidy/break to alleviate pain

France just did this, handing out a $100 energy cheque to 38 million people, capping gas prices, and setting limits on electricity price increases.4 That definitely sounds like a sustainable solution 🙃. But it just goes to show my point that this will not stand - if the first fix is to give everyone a cheque, you can make a bet that officials and organizations are going to influence prices, even in a very irrational way. And that can have dramatic impacts. We have seen something similar from the UK as well.

From a recent WSJ article:

“Europe is particularly dependent on Russian diesel and prices there leapt after the invasion. The rise added to existing pressures on consumers and businesses, and prompted governments in the U.K., France and elsewhere to reduce sales taxes for road fuels.”

Conclusion

In the short term, Oil and Gas companies are going to be reaping some great benefits. Ramping up their balance sheets and expanding good margins. I think there is a window for this, but in the mid to longer term, I find it hard to see how we sustain these prices given the nature of the causes of these increases. I would have made an argument for the inflationary costs hitting the servicing and producers, but this excerpt from the recent Kinder Morgan earnings call made me think twice:

“The second thing is we haven't experienced a great deal of inflation to date. We experienced as normal when the commodity prices are up, you see it in the oil field, right? But commodity prices are up. The revenues are up to go with it. So we're seeing some there.

The other places where we're seeing inflation, we projected a little inflation, but the places where we've actually experienced it are obviously fuel for our trucks, okay, and for our other equipment. So fuel prices are up, those prices are up. Related hydrocarbons or composites like lubricants is also up. And some materials, steel costs for certain equipment has come up. And even though raw steel has come down a little bit, it's been down, then up a little. So it's some materials, equipment, lubricants fuel.” - Kinder Morgan Q1 Earnings Transcript

So if we are thinking big picture and any of these components shift :

Expansion of Chinese demand and/or security-based purchases

EU countries giving in to Russia’s demands

Governments enforcing methods to curb prices

Increase in global production

We are going to see some movement, and that Urals-Brent discount might just compress, with lower prices across the board as existing supply finds some new, and familiar homes.

https://context.capp.ca/articles/2020/pirl-fertilizers/

kpler.com/blog/russian-oil-exports-continue-for-now-despite-trading-constraints-and-declining-vessel-availability

https://www.wsj.com/articles/russias-oil-industry-linchpin-of-economy-feels-sting-of-ukraine-war-disruptions-11649843249

https://www.rfi.fr/en/france/20220126-france-to-help-drivers-stave-off-cost-of-soaring-fuel-prices