The dragon tries to roar

Or ... is China waking up from its Covid nap ?

This week we were fortunate to have Altenomics covered on the Alternative Data Podcast (I talk about ESG then get into it) this week and to also have our inflation article cross-posted by CAIA.

The interlinkages of the world China

You have to really take a pause sometimes and reflect upon the fact that in times of extreme health and safety concern, our primary global pressure seems to be how fast we can open up to get people spending again. It’s just a big fallacy of the economic world that humans designed. But hey, that’s the rules of the game - let’s talk about Chinese demand and supply…

Per Bloomberg:

China’s lockdowns to contain the country’s worst Covid outbreak since early 2020 have battered the economy, stalling production in major cities like Shanghai, and halting spending by millions of people shut in their homes.

The restrictions are intended to eradicate any trace of the virus in the community, but they’ve also pressured everything from manufacturing and trade to inflation and food prices.

That’s the nature of our societies and the cascading effects of globalization and complexities of global supply chains.

We are only as strong together these days as our weakest, or most constrained link - and that’s why this all matters. China currently consumes more than half the world's copper and steel supplies, and it accounts for well over half the world's primary aluminum production. That for a country that is 19% of the global population.

As a result - when they shut down, supply chains get disrupted fast.

Open for business

As of today, Shangai is officially open for business after an incredibly intense shutdown. To truly understand the extent of those lockdowns, check this thread out:

The short of it, which I have seen through from social posts, and chatting with colleagues of mine in Shangai is that there are barricades everywhere, and people are having to self organize to buy food in bulk as apartment blocks - just crazy stuff.

Overall - it appears that they have effectively brought down their case counts. The Covid-Zero Strategy is widely believed to be the single biggest drag on global growth at the moment - but perhaps this is now the end of it - with ‘normal life resuming’ starting today.

What is it going to take to get back to production?

Let’s paint some colorful pictures, shall we? The charts below are a measure of the air quality index for Shangai. Air quality can be used as a proxy for economic activity.

So what?

China is not yet close to pre covid levels, fortunate for the environment I suppose - but not for the global economy. However, we can see that December and January were relatively strong before the Major outbreaks in March which subsequently caused the lockdowns.

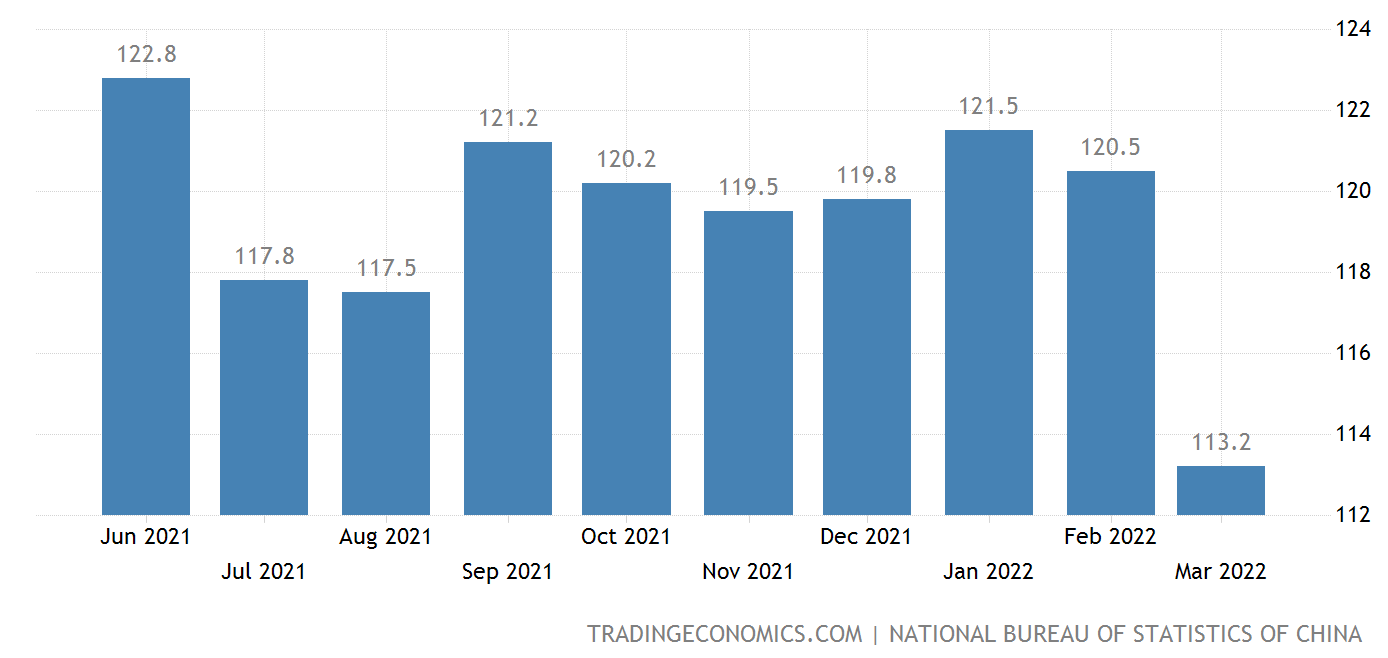

Statistics China runs the Chinese Consumer Sentiment Survey monthly, and the most recent reading got some negative headlines. The large drop to 113.2 for March was more drastic than many thought.

But if we zoom out a little bit, we see that it’s relatively similar to the early days of Covid. With restrictions now being eased, supposedly - this may start to shift the demand side of the equation.

This data is from AutoNavi - a commonly used Chinese GPS/map service - which shows a similar trend, basically, the result of Chinese lockdowns brought things to a halt not seen (even more so in Shanghai) since the early days of Covid in 2020. But again, everything points toward the lows being behind us - as they get back on track.

Bottomline - the dragon awakens, and with this comes the reconstruction of the global supply chain. No one knows if it will be a false start, and it very well might be as reopening results in additional cases, and Chinese officials prioritize the people over the economy - to the extent they can.

However, the low points seem to be behind us, and we should continue to see increased Chinese demand for energy and commodities, and with that, the supply of global goods can start to resume. Many positive feedback loops to come from this as more materials and parts are available, hopefully starting to drive prices lower and combat the worldwide inflation, although, in the short term, some of this may get worse before it gets better (e.g energy) as capacity ramps up.

Shipping containers are a good first sign of this:

As usual, I am a serial optimist - but I believe in the natural instinct to heal and recover. We seem to be on that path, but not out of the woods yet.

Thanks for reading, if you enjoyed this please consider sharing this post on social media or with your friends.

Keep pushing forward.

Qayyum Rajan, CFA