[G]rate Expectations

or what is a 'soft landing' anyways ?

It’s that part of the economic cycle - a little different every time, with some surprises - but it is time for rate hikes. Whether these stay for the long haul, or if they are just being put up while they can, creating some buffer room (remember early 2020) - all eyes and ears are on the Fed.

75 bps or nah?

Powell, in the most recent FOMC meeting, said that a 75bps rate hike was off the table, and yet the market seemed to think otherwise, assigning probabilities of some aggressive rate hikes into 2023, at which point it is expected to taper off.

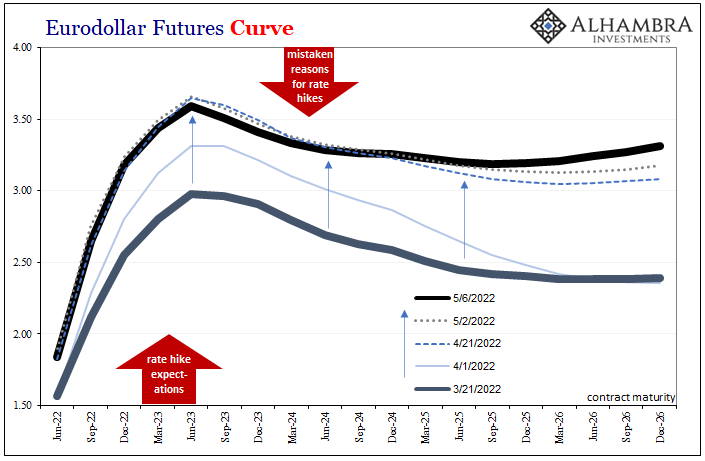

The current projected path (i.e what’s being priced in) is based on things like the Federal Funds Futures. I took the liberty of charting out the existing contracts to have a look from last week to today:

Effectively, we see a large hiking cycle into mid-2023 before we start to see some easing. This is what the market is pricing, not necessarily what the Fed has said - this is an important point.

The uncertainty is palpable. For various reasons:

It is unclear how “soft” the landing will be from the expected hikes

It is unclear how the fed will react to the cascading effects of these expectations

It is unclear how the fed will react if all of a sudden we see inflation reduce significantly

This uncertainty is reflected in the shapes of these implied curves over the last few weeks as we start to truly understand where the actual path may be. There are many known unknowns, but also unknown unknowns, so you can expect these to shift over time.

All of this means that there is opportunity in chaos.

Markets have tanked, bonds have tanked, inflation continues - and now the question becomes, how much carnage is acceptable - and how long before the Fed through financial pressures and systemic risk, or via politics - decides to do a u-turn.

This is the trade, and the thought. It’s not about whether interest rates are going up and down, it is about when they are going up when they are going down, and are current market expectationss priced correctly?

In my view - markets have over-indexed.

Over in eurodollar futures, its curve has essentially moved itself upward as the FOMC reveals itself to be more hawkish. The shape from before late April has been revisited in early May. Still wildly inverted, yet the whole curve moved higher nominally given a more aggressive hawkish stance on hikes.

This is likely because Fed policymakers, Mr. Powell in particular, have made it perfectly clear (press conference) that rate hikes aren’t really attached to economic conditions. Yes, that’s what he said and “they” will continue to say, that hikes are in response to inflation plaguing an otherwise awesome economy, but that’s not what’s going on here as the balance of market positions will attest.

The excellent chart above is similar to the one I showed earlier and this was leading up to the first week of May. As meetings got closer, rate expectations went up significantly, but have now come down since that initial peak of 3.5% to just under 3% as an implied rate at the end of Q1’23.

It's refreshing to write altenomics bi-weekly because we get to see things develop a little bit more in real-time and settle in, vs day to day commentary. As I saw Powell make that speech, the first thing I thought of was that futures have to be readjusting to this, because hey, the fed told us what they were going to do. Expectations did indeed drop, but then rose again - which is when we went long March 2023 Eurodollars - where rates are supposed to be at their zenith before dropping.

This is a great chart showing market expectations at the start of historical hiking cycles…

Here is the actual Fed Funds Rate overtime.

You can look at each one of those paths, and see what actually happened. The Dot-Com bust, 2008 MBS issues, Covid-19 - the world just doesn’t work on straight paths, there are a lot of zigs and zags as we adapt to changes on earth.

Stimulus Junkies 💉

As you can see, the discussion is far from over, because of the uncertainty that exists.

Markets have basically been heroin addicts in the advent of historically low rates, which have allowed immense issuing of debt, and many business models that rely on this that tend to get hammered when rates increase (i.e big tech). I always get a bit of a sick feeling watching this video, meant to display addiction - but I think it is a good analogy for the predicament of the current financial ecosystem. The nuggets are stimulus and easy money.

Don’t take my word for it, there was a video going around a few days ago, but it seems to be removed across the internet. It was an interview with Richard Fisher (former Fed president) from a few years back.

"I like to say that we injected cocaine and heroin into the system, and now we're maintaining it on Ritalin. How's that? {Laughs)"

- Former Dallas Federal Reserve President Richard Fisher

We just had a relapse, I don't know if we are ready to kick it just yet.

The interesting thing about this is that depending on political, social, and market pressures - it can come in many ways. Zero Hedge said it best:

Condition me, baby.

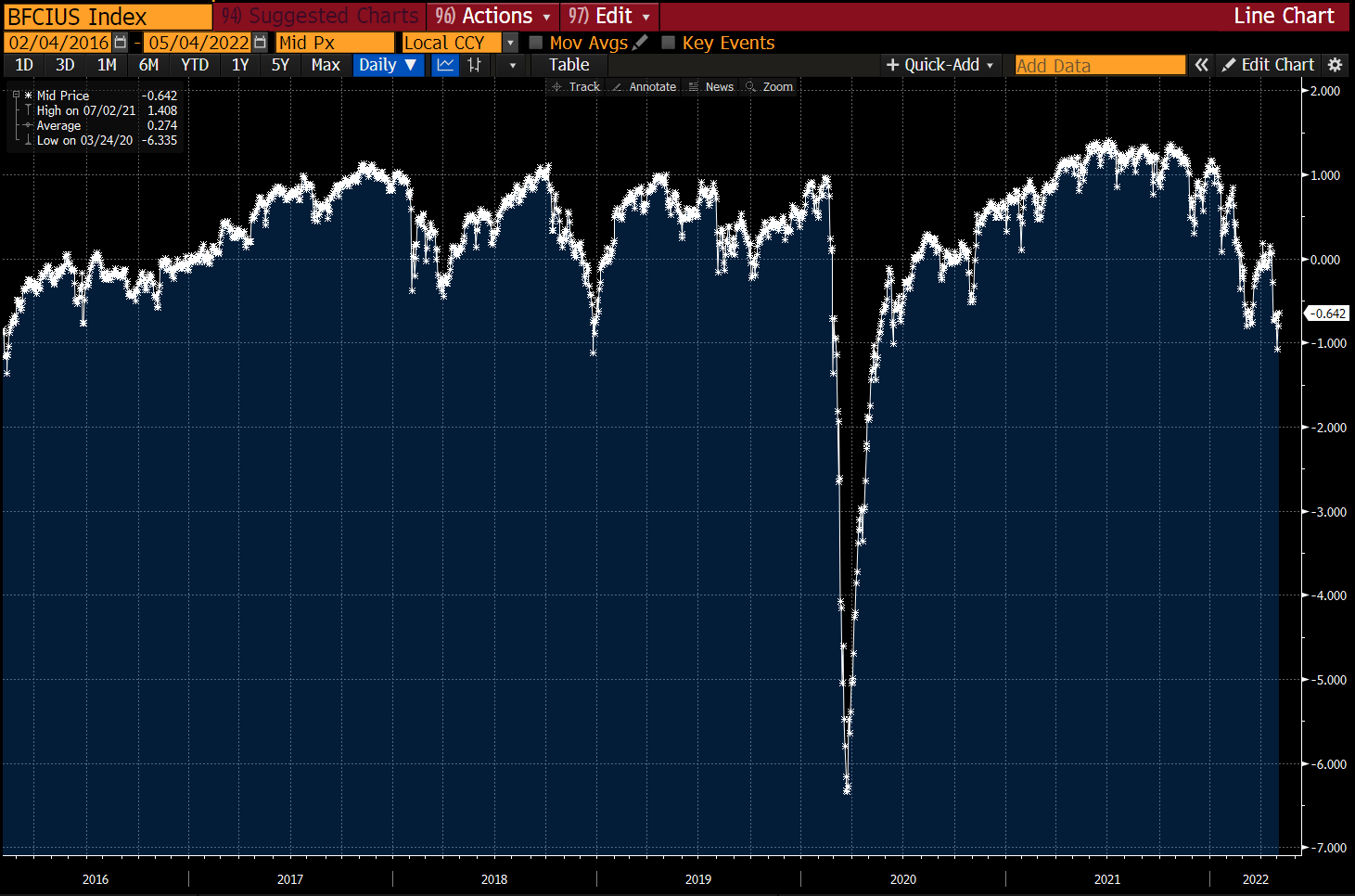

Let’s talk financial conditions. Financial conditions indexes are created in many forms, and they take in a bunch of variables that relate to the supply and demand of economic activity. Are they perfect? No, but they give some useful indications.

The bond market is telling us, that things are about to get worse, for financial assets anyhow. The Fed will try to hike as much as it can, while it can - a safety net for any future cuts they might need to make.

But then there's going to be a breaking point, and well, we know that when enough noise is made - the Fed will do what's necessary.

Here is the Bloomberg Financial Conditions Index - last 2 years. Negative values indicate tighter conditions.

This is the FCI from the Chicago Fed - negative values indicate looser conditions

The goal here for the Fed is to tighten conditions enough to slow inflation. Interestingly enough, you can see from the Bloomberg FCI that even though conditions have tightened a lot, it is not even close to the tightness at the peak of the pandemic.

It is truly a balancing act. Make things too tight, and we have a massacre on our hands - and that will require a bit more stimulus, or expectation of not as much tightening.

The question: Have we tightened enough to slow inflation? I continue to believe that we have, with what markets are pricing in, along with the fact that so much of this inflation, in my view is from elements that can change quickly, and have a high potential for reflexive action, we cover these here:

A shortened flight path

Even though Powell says that it doesn’t matter, I think we have a lot of things that the world is trying to figure out.

Inflation expectations

Market crashes / prolonged pain - how low can we go?

Deteriorating financial conditions

Looking 1 year in at Eurodollars gets really interesting - assuming they can't make that work. The peak of March/June 2023 is the supposed peak, and if markets make the Fed cut at all, or they are not able to go as sharp as they want, that’s a big win. On the other hand, it is unlikely they will try to raise even more than is currently projected, as that will do nothing but destroy whatever semblance of a soft landing there is. From a risk/reward perspective - checks out.

All of this being said, I have always believed that the lack of easy or cheap money is ultimately good for markets and the world in general. When we stop manufacturing artificial growth, such as buybacks - and the cost of capital is slightly higher, then businesses have to take more risk, to engineer the same or higher returns. Right now, the irony of a stimulus, is that it creates risk-averse organizations. But when you shake things up, well, that’s when we get innovative and see those TFP gains in GDP.

Thanks for reading!

Qayyum “Q” Rajan, CFA